WIIFY (what’s in it for you) with this post? Learn or refresh yourself on budgeting (and its counterpart – actual spending) from the Budget Teeter-totter!

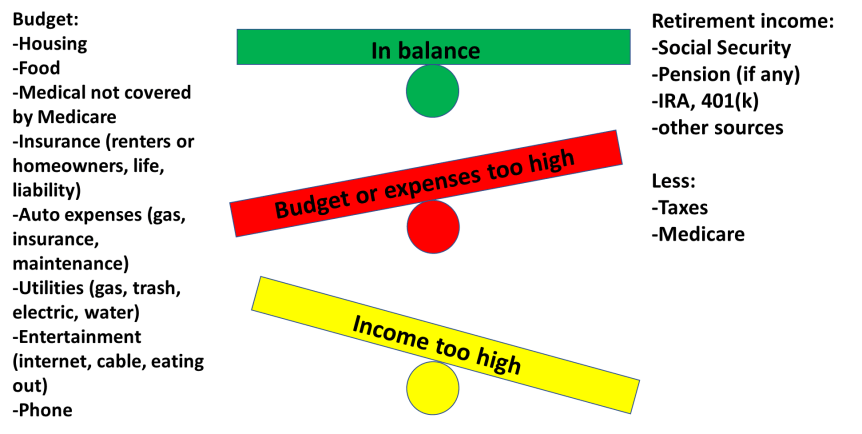

Budget Teeter-totter

Budget Teeter-totter quick guide

Green – good – expenses and income in balance.

Red – bad – expenses exceed income.

Yellow – good and bad – income exceeds expenses but may cause ‘surprises’ with income or estate taxes.

Good news-bad news-good news

I’ve got good news and bad news and good news. The good – you’re retired or thinking about it and want the best you can attain. The bad – if you’re like 99% of us, you’re going to be on what’s called a ‘fixed income’. The other good news is that with planning, prioritizing, and budgeting, you can avoid surprises!

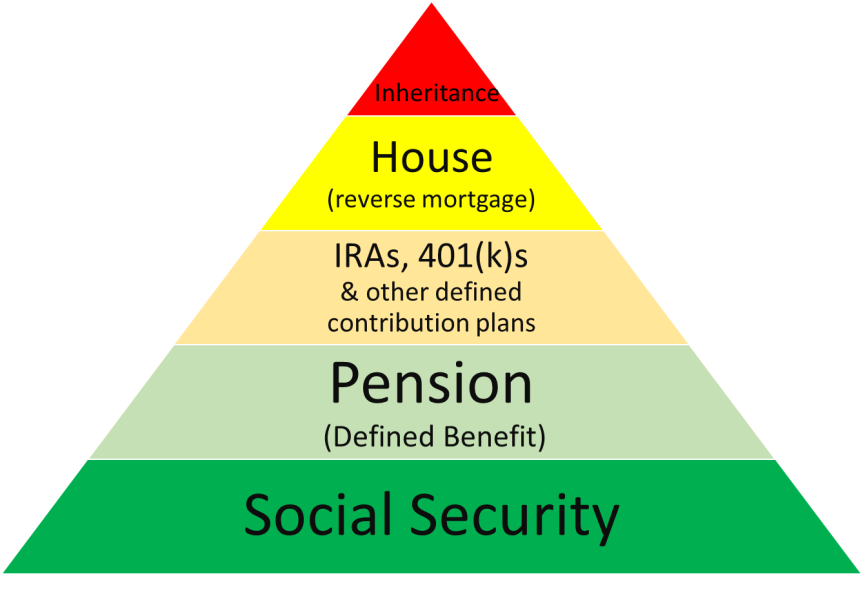

Two pieces to planning – income and expenses

Bottom line from this section – know your planned income as it will dictate what you can spend without ‘surprises’. www.ssa.gov has a retirement estimator that you (and your spouse if you have one) can estimate your Social Security benefits. You will also need to estimate your income from any pension and IRAs/401(k)s/403(b)s and don’t forget required minimum distributions (RMDs). Lotta letters/numbers there… Frankly, if you don’t do this a lot, you might want to strongly consider a trusted financial professional. Designation Check can help you find a Chartered Financial Consultant (ChFC) and here’s a place to find a Certified Financial Planner (CFP) finder. On my personal income side, I include Social Security, a small pension, 401(k), and savings. I reduce the income by my forecast of Federal and State income taxes.

Bottom line from this section – know your expenses and have a budget that leaves you in the green (or yellow) on the Budget Teeter-totter. On my expense budget side I include:

-Utilities – gas, electric, water, phone/internet/TV (too much!), cell phone, trash, homeowners association dues

-Forecast medical insurance expenses (if I retire pre-65 COBRA or exchange rates, post-65 a Medicare supplement)

-Property tax

-Car licenses

-Homeowners insurance

-Car insurance

-Personal insurance (life, LTC)

Actions you can take:

-Learn about RMDs. IRS RMD information.

-Start researching your retirement income and/or budget.

-Let me know in the comments or via ‘Contact’ what else you’d like to see in the expenses.

Up next – You’re gonna die! But we can help with a surprise there, too. Look for the next update on Friday, July 21 at 12:30 PM.

Questions, comments, or suggestions for retirement surprise areas you want to know more about?

-Leave a comment

-Use ‘Contact’, above, to send an email.